+55-11-3280-2197

+55-11-3280-2197 +1-305-851-7982

+1-305-851-7982 +44-020-8144-4939

+44-020-8144-4939

Rio de Janeiro

Av. Presidente Wilson, 231 / Salão 902 Parte - Centro

CEP 20030-021 - Rio de Janeiro - RJ

+55 21 3942-1026

Although the creditor has the guarantee of the debtor's complete assets, or that of specific assets (through a mortgage or pledge), this does not mean that they can seize any of the assets owned by the debtor, or specific assets affected, but will have to follow certain procedures to compensate for unpaid debts.

In the event of non-payment, the usual thing is for the credit institution to try to recover the sums owed (principal, ordinary interest, late payment interest, commissions, expenses) in a friendly manner. When the debtor does not agree to this friendly solution, or when circumstances make this type of solution impossible, the creditor will initiate legal actions.

These actions will in turn be conditioned by the type of title that protects the creditor's credit, depending on whether we are dealing with executive or non-executive titles.

The executive title allows the direct judicial claim of the credit, resorting to the executive judicial procedures. This would be the case of a loan formalized in a notarial deed or policy.

The non-executive title is not sufficient for the direct judicial claim of the credit, but requires the prior judicial recognition or declaration of the creditor's credit. An example of a non-executive title would be the savings book opening contract in the event of an account overdraft that is not voluntarily regularized by the customer, or a card issuance contract not formalized in a notarial instrument. Therefore, you must go prior to a declaratory judicial procedure. Once the creditor has the judgment that recognizes his credit against the debtor, he may resort to the executive route described in the previous paragraph.

As a result of the differentiation between executive and non-executive title, it turns out that it favors the creditor to have an executive title, since their judicial claim will be processed more quickly, and with fewer possibilities of opposition on the part of the debtor, since in the creation of the title Specially qualified public notaries have intervened (notaries, property registrars, judges, etc.) who ensure their formal correction and the balanced defense of the rights and obligations of the parties, subject to the Law.

Monetary debts that are not contradicted by the debtor can be notarized, in order to obtain by the creditor a payment letter voluntary or an extrajudicial executive title to which the debtor may oppose, where appropriate, through the courts. Claims involving a consumer are excluded from this channel, among others. It is considered that this new way of claiming liquid amounts already overdue and not paid can contribute to a significant decrease in the volume of cases that are filed annually in the courts, by becoming an alternative to claiming debts through the courts.

Classification of judicial procedures for debt recovery.

The declarative procedures are the monitoring, the verbal and the ordinary.

The executive procedures are the exchange rate and the execution procedure.

Payment for payment process. Through the order for payment process, another may be required to pay a monetary debt, due and enforceable, of any amount, when the debt of that amount is accredited by documents, whatever its form and type or the physical medium in which it is found, that appear signed by the debtor or with his seal, imprint or brand or with any other signal, physical or electronic, from the debtor, or by means of invoices, delivery notes, certifications, telegrams, faxes or any other documents that, Even though they are unilaterally created by the creditor, they are one of those that habitually document credits and debts in relationships of the kind that appear to exist between creditor and debtor.

The amounts owed for common expenses of communities of urban property owners may also be claimed through the order for payment process.

If the debtor opposes the initial writing of the creditor, the matter will be definitively resolved in the corresponding trial.

Verbal judgment. It is a simple procedure, in which the concentration of the actions is maximum. Likewise, a greater speed is sought in its processing, under the criterion of the simplicity of what is discussed and its economic amount.

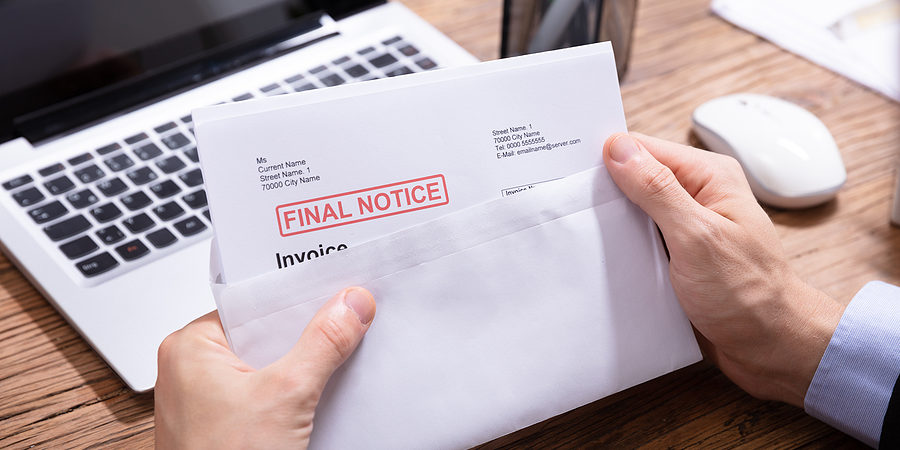

Avoiding default in the company is a major concern among entrepreneurs and financial institutions, especially in times of crisis, where the rate of customers who are unable to pay their debts tends to increase.

Default and credit recovery for your company

For this, a good preventive action is essential to avoid measures of credit recovery in arrears before the courts. Through a series of methods it is possible for the creditor to avoid litigation and seek to negotiate its receipt with the debtor, reducing default. At this point, the need arises to know how to deal with different types of debtors and how to make a good credit recovery without losing your customers.

To resolve this and other doubts, the topic of today's conversation will be the recovery of credits in an extrajudicial or judicial way as a solution to the default in the company. So if you want to know more about this subject, you are in the right place!

How does overdue credit recovery work? How can a law firm help me with this?

How Credit Recovery Works

To explain how credit recovery works, it is important to first clarify the difference between default, extrajudicial collection and legal proceedings. The extrajudicial charges are only intended to recover the amount due from the customer even before the filing of an action or simply a renegotiation of debts with a better guarantee. Eventually there may be an attempt to negotiate with flexibility, to facilitate the payment of the debt, such as installments and discounts. Thus, the customer gets rid of the default in the company and clears his name, being able to buy again. The recovery of overdue judicial credit seeks to sue the debtor in court, in many cases already reaching his assets or guarantees already provided with the inclusion of fines, corrections, legal costs and attorneys' fees.

To carry out this operation, we recommend the help of a law firm, as the knowledge of a lawyer specialized in civil and civil procedural law is essential both in the negotiations stage, where it is important to provide support as to the legal path to be taken in relation to the debt collection, as well as in relation to the laws that govern the law applicable to the specific case, in order to reduce bureaucracies in the process and face the slowness of Brazilian justice.

Some of the benefits of seeking legal advice to recover credit are:

Knowledge of procedural, civil, commercial and sparse laws avoids problems with creditors trying to recover claims that sometimes do not meet the requirements for a faster and more efficient process.

Location of assets and analysis of guarantees that pay the full amount of the debt in the event of default by the client;

Dismantling of structures commonly used for concealment of assets;

In the case of legal entities without assets in their name, it is requested to disregard the legal entity to search for the assets of the partners that can settle the debt.

Types of credit recovery: what are they and how do they work?

Types of Credit Recovery

When it comes to defaults and credit recovery, it is important to mention the two types of credit recovery: extrajudicial (or amicable) and judicial collection.

Extrajudicial recovery is the fastest and least costly method, seeking to negotiate when in direct contact with the client through specialized advice, whether from the company itself, outsourced or even through lawyers. Here, discounts, installments and other ways of renegotiating the payment of the debt are offered. The contact can be made through several ways, such as e-mail, phone calls, messages ... The objective is to offer the creditor the payment of what is due to him and at the same time to the debtor the most appropriate method for the settlement of his debt, maintaining its name clean and preserving its purchasing power, which allows the customer to return to do business with the company!

Judicial collection is used only when the negotiation methods have failed and the company is at risk of losing and not recovering credit due. It is the slowest and most bureaucratic solution, due to the slowness of Brazilian justice.

It is necessary to contact a team of lawyers specialized in civil procedural law and overdue credit recovery in order to resolve defaults in the company.

The judiciary will send letters of summons to debtors and it is possible that the consumer's name will be immediately placed on the lists of credit protection agencies such as SPC and SERASA or even if the latter has his assets confiscated for the payment of the debt, in case of a lawsuit. of execution.

How to deal with the 4 types of debtors?

o dealing with customers who are in default in the company, it is important to have a profile analysis in order to know how to qualify the customer regarding the types of debtors. Such an analysis is important to decide the method of approach adopted, always remembering that in every credit operation, a prior risk analysis as well as offering payment guarantees is necessary. Check out:

1 - Occasional debtor: He does not usually delay or fail to pay, with his delays normally being related to unexpected problems that lead him to prioritize another payment or forget some due date. They tend to pay as quickly as possible.

The approach must take into account the customer's history. This credit is easy to recover. It is important to maintain the relationship with consumers who have this type of profile. Approaches of wrong tone can leave you very dissatisfied, causing the loss of the client. Advantages such as interest discounts are attractive to this type of consumer.

2 - Chronic debtor: Characterized by the poor organization of his finances, this type of client often misses deadlines.

Although it often pays only after the entry of effective collection actions, it should not be approached as a bad payer. As much as he demands frequent collection actions, he still pays, even with a fine and interest. The approach must be straightforward, but not too incisive. Despite the delays, it still generates financial returns.

3 - Negligent debtor: He has total lack of control over his finances, buying more than he can afford. Generally, it is unable to pay the debt in the short term, requiring a more incisive approach. It is necessary to offer adequate conditions to recover credit.

4 - Bad payer: They are more resistant to collection actions, because for them the non-payment of their debt is not a problem. Normally, they have already fully shielded their assets and do not have assets capable of resolving the debt.

They demand a more incisive and direct tone in the approach. As the interest in maintaining the relationship with this client profile is low, the most effective actions involve making it clear that judicial referral is a real possibility.

Mr. Alessandro Jacob speaking about Brazilian Law on "International Bar Association" conference

Mr. Alessandro Jacob speaking about Brazilian Law on "International Bar Association" conference Av. Presidente Wilson, 231 / Salão 902 Parte - Centro

CEP 20030-021 - Rio de Janeiro - RJ

+55 21 3942-1026

Travessa Dona Paula, 13 - Higienópolis

CEP -01239-050 - São Paulo - SP

+ 55 11 3280-2197